- A bumper year: In 2019, gross financial assets jumped by 9.7% and reached EUR 192 trillion

- Crisis? What crisis? Global financial assets increased by 1.5% in the first six months of 2020, driven by fast rising bank deposits

- Trend reversal: The wealth gap between rich and poor countries has widened again

- Asia: Back on track

SINGAPORE, 24 September, 2020: Today, Allianz unveiled the eleventh edition of its “Global Wealth Report”, which puts the asset and debt situation of households in almost 60 countries under the microscope.

A bumper year

Never in the last ten years, we were able to report such a big increase in wealth: Worldwide, gross financial assets[1] grew by 9.7% in 2019, clocking the strongest growth since 2005. This performance is nothing but astonishing given the fact that 2019 was marred by social unrest, escalating trade conflicts and an industrial recession. But as central banks reversed course and embarked on broad-based monetary easing, stock markets decoupled from fundamentals and soared by 25%, lifting financial assets in the process: The asset class of securities increased by a whopping 13.7% in 2019; never was growth faster in the 21st century.

The growth rates of the other two main asset classes were lower – but still impressive: Insurance and pensions reached a plus of 8.1%, mainly reflecting the rise of underlying assets, and bank deposits increased by 6.4%. In fact, all asset classes clocked growth significantly above their long term averages since the Great Financial Crisis (GFC).

Another peculiarity of 2019: Through all the years, the regional growth league table used to be dominated by Emerging Markets. Not so in 2019. The regions that saw the fastest growth were by far the richest: North America and Oceania where gross financial assets of households increased by a record 11.9% each. As a consequence, for the third year in a row, Emerging Markets were not able to outgrow their much richer peers. The catch-up process has stalled.

Crisis? What Crisis?

The same story is about to repeat itself in 2020 – but only in extreme. As Covid-19 plunged the world economy in its deepest recession in 100 years, central banks and fiscal authorities around the world fired up unprecedented monetary and fiscal bazookas, shielding households and their financial assets from the consequences of a world in disarray.

We estimate that private households have been able to recoup their losses of the first quarter and recorded a slight 1.5% increase in global financial assets by the end of the second quarter 2020 as bank deposits, fueled by generous public support schemes and precautionary savings, increased by a whopping 7.0%. Very likely, private households’ financial assets can end 2020, the year of the pandemic, in the black.

“For the moment, monetary policy saved the day”, said Ludovic Subran, chief economist of Allianz. “But we should not fool ourselves. Zero and negative interest rates are a sweet poison. They undermine wealth accumulation and aggravate social inequality, as asset owners can pocket nice windfall profits. It’s not sustainable. Saving the day is not the same as winning the future. For that, we need more than ever structural reforms post Covid-19 to lay the foundations for more inclusive growth.”

Trend reversal

The wealth gap between rich and poor countries has widened again. In 2000, net financial assets per capita were 87 times higher on average in the Advanced Economies than in the Emerging Markets; by 2016 this ratio had fallen to 19. Since then, it has risen again to 22 (2019). This reversal of the catching-up process is widespread: for the first time, the number of members of the global wealth middle class has fallen significantly: from just over 1 billion people in 2018 to just under 800 million people in 2019.

Looking at the development since the turn of the century, however, the rise of Emerging Markets remains impressive. Adjusted for population growth, the global middle wealth class grew by almost 50% and the high wealth class by 30% – while the lower wealth class declined by almost 10%. Despite this progress, the world remains a very unequal place. The richest 10% worldwide – 52 million people in the countries in scope with average net financial assets of EUR 240,000 – together own roughly 84% of total net financial assets in 2019; among them, the richest 1% – with average net financial assets of above EUR 1.2 million – own almost 44%.

The development since the turn of the millennium is striking: While the share of the richest decile has fallen by seven percentage points, that of the richest percentile has increased by three percentage points. So the super-rich do indeed seem to be moving further and further away from the rest of society.

“It is quite worrying that the gap between rich and poor countries started to widen again even before Covid-19 hit the world”, commented Michaela Grimm, Allianz senior economist and co-author of the report. “Because the pandemic will very likely increase inequality further, being a setback not only to globalization but also disrupting education and health services, particularly in low-income countries. If more and more economies are turning inwards, the world as a whole will be a poorer place.”

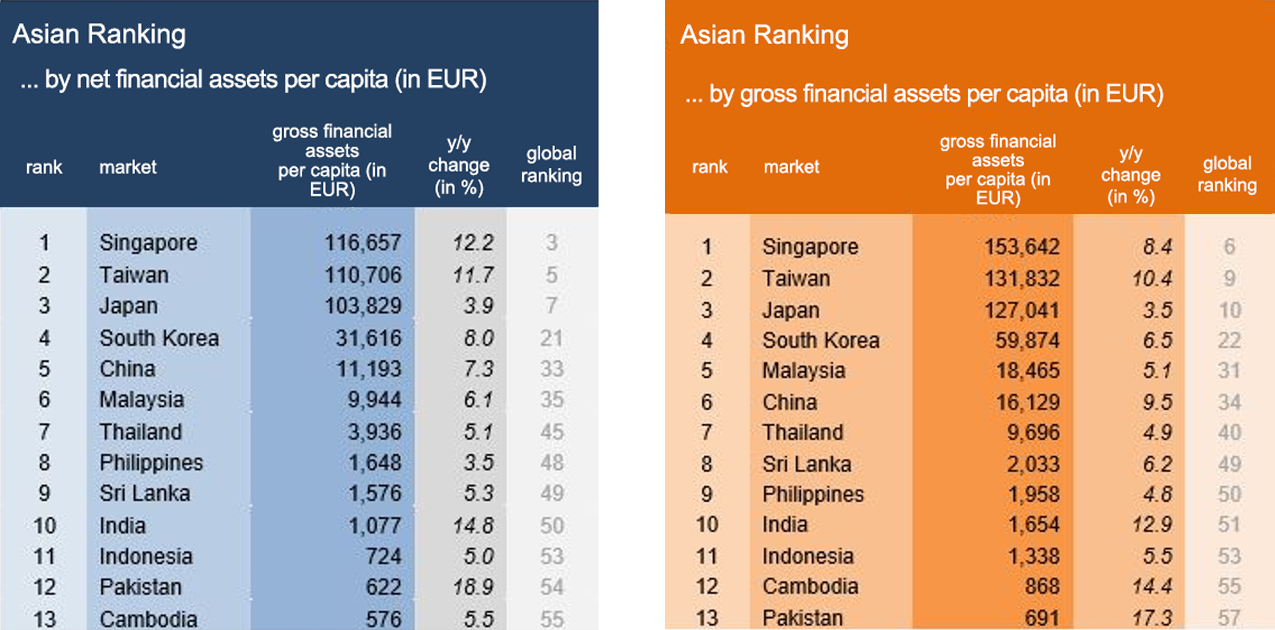

Asia ex Japan: Back to track

After dismal growth in 2017 (a mere +5.5%) and a decline in 2018 (-1.2%), gross financial assets of Asian households rose by a healthy 9.9% in 2019; this was, however, the third slowest increase since the GFC. With rising wealth in the region, double digit growth rates become more difficult to achieve. All asset classes contributed to the recovery: bank deposits clocked growth of 11.0% and insurance and pension growth of 12.7%, both easily beating the global average.

Securities, on the other hand, increased by a more modest 7%, well below the global average of 13.7%, reflecting the somewhat weaker stock performance in the region. Almost all countries in the region grew faster in 2019 than in 2018, with China, India, Taiwan and Cambodia setting the pace with double-digit increases.

In contrast to assets, liability growth slowed down further, growing by 11.8% in 2019, the weakest increase since the GFC. The debt ratio (liabilities in % of GDP), however, continued to climb and reached 55.1% at the end of 2019, almost twice the level seen immediately after the GFC.

Net financial assets, finally, increased by 9%. With net financial assets per capita of 6,700 euros, the regional average is well above that of other emerging regions such as Latin America (EUR 5,954) or Eastern Europe (EUR 5,157) – but still well below the global average of EUR 26,411.

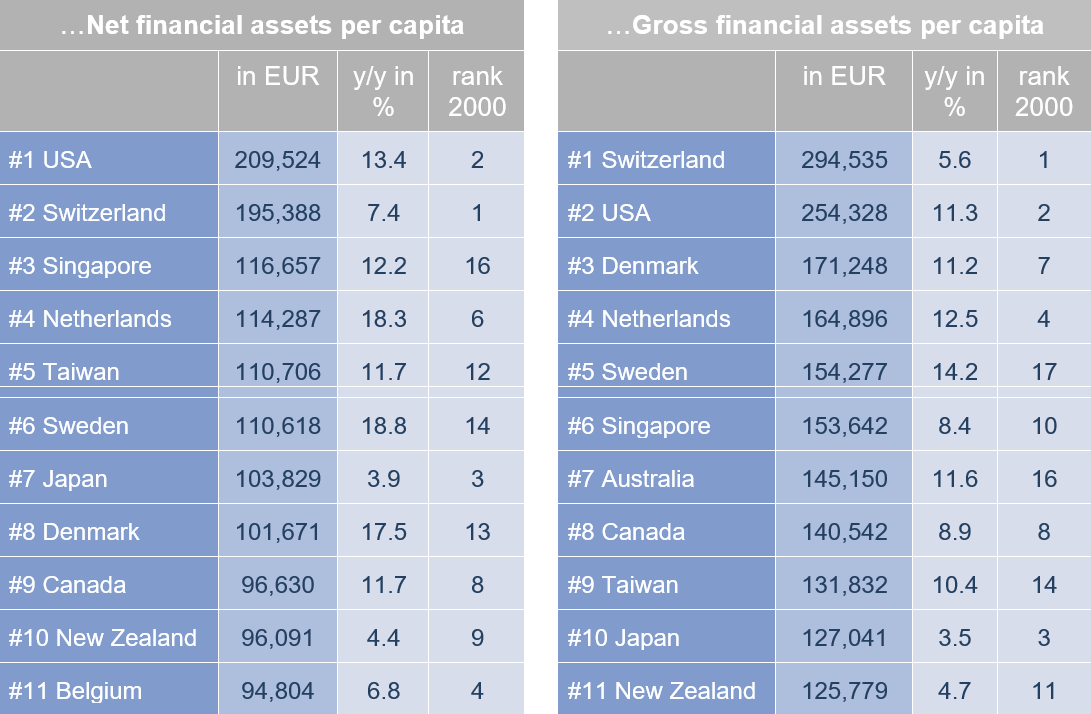

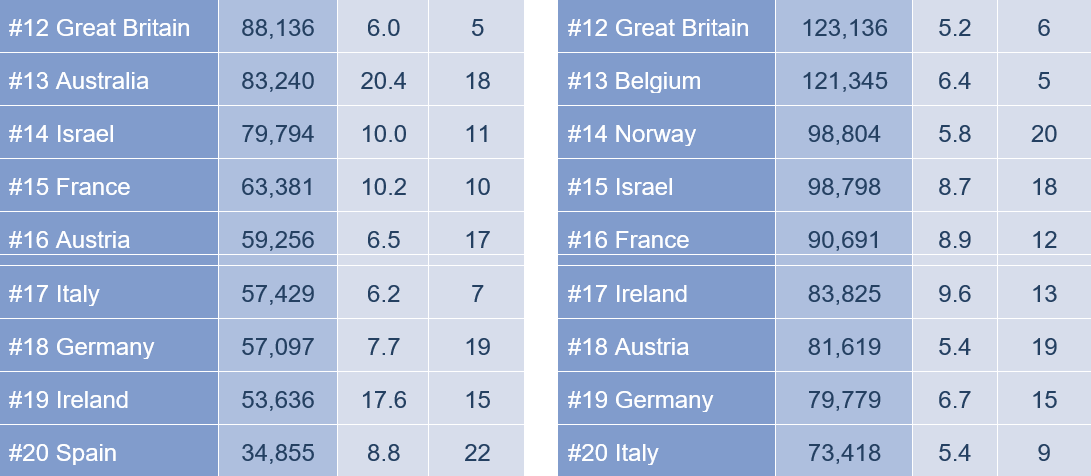

Top 20 in 2019 by...

[1] Financial assets include cash and bank deposits, receivables form insurance companies and pension institutions, securities (shares, bonds and investment funds) and other receivables.

You can find the study here on our homepage

For further information, please contact:

Singapore: Sean Ottley, sean.ottley@allianz.com.sg, +65 8614 0997