- Over the next decades, baby boomers will retire en masse and put social security system under severe stress

- Only a handful of countries have already made their pension system demography-proof, above all Sweden, Belgium, and Denmark

- In most other countries pension systems will struggle, beset with high public deficits and an uneven balance between sustainability and adequacy – tilted in most cases in favor for the latter

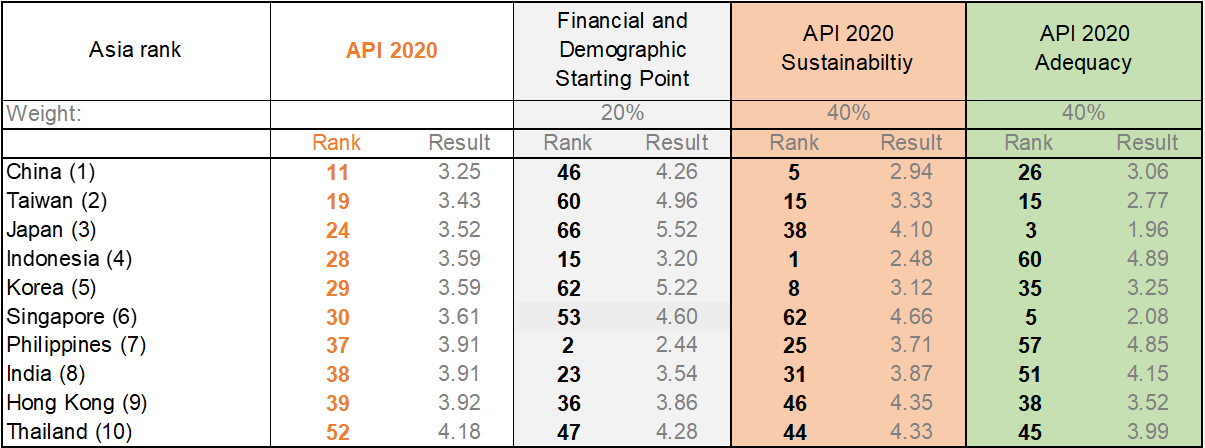

- No Asian market ranks among the top-10 – against the backdrop of rapid aging in the region, a lot of homework remains to be done in terms of pension reforms

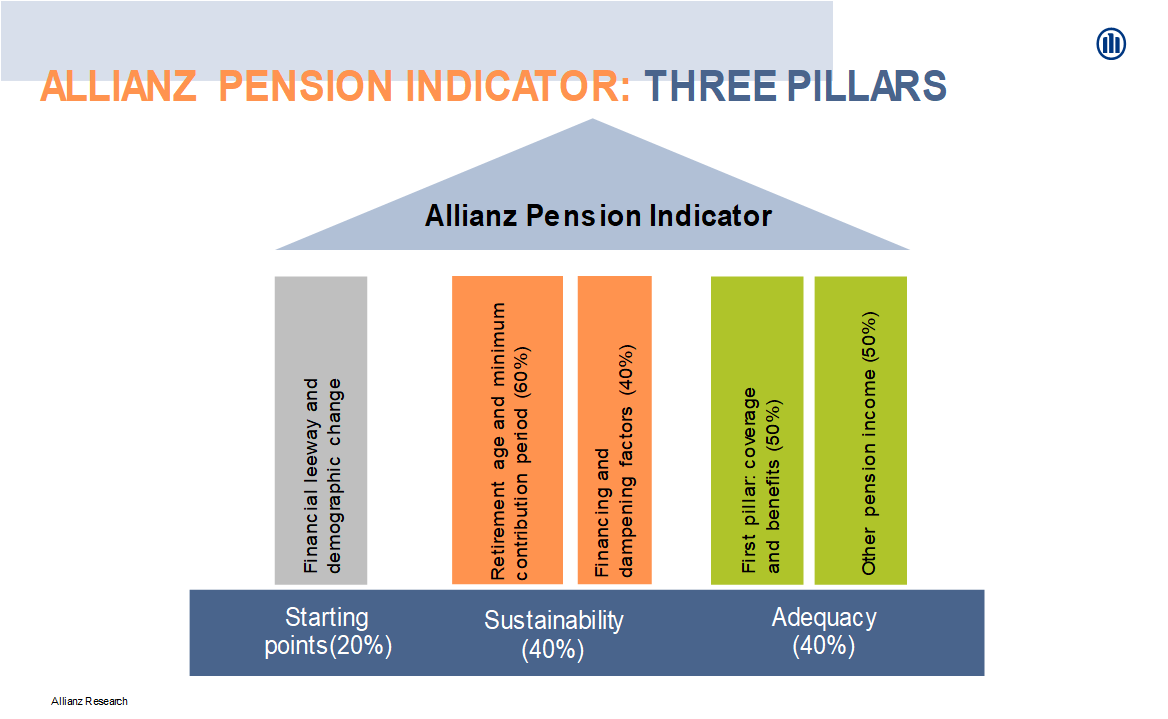

SINGAPORE, 29 May, 2020: Today, Allianz unveiled the first edition of its “Global Pension Report”, taking the pulse of pension systems around the world with its proprietary pension indicator, the Allianz Pension Indicator (API). The indicator follows a simple logic: It starts the analysis with the demographic and fiscal prerequisites and then continues to examine pension systems along their two decisive dimensions: sustainability and adequacy. Hence, it is based on three pillars and takes all in all 30 parameters into account, which are rated on a scale of 1 to 7, with 1 being the best grade. By adding up all weighted subtotals, the API assigns each of the analyzed 70 countries a grade between 1 and 7, thus providing a comprehensive view of the respective pension system.

“Demographics and pensions have been eclipsed by other policies in recent years, first and foremost climate change and today the fight against Covid-19”, said Ludovic Subran, chief economist of Allianz. “But you ignore demographics at your own peril, demographic change will soon be back with a vengeance. Defusing the looming pension crisis and preserving generational justness and equality are key for building inclusive and resilient societies.”

The dramatic shift in demographics is best characterized by the increase in the global old-age dependency ratio[1]: Until 2050, it will grow by a whopping 77% to 25%, i.e., faster than in the last 70 years since 1950. In many emerging economies the ratio is going to more than double within the next three decades, that is, in less than half of the time this development took in Europe and Northern America. The most prominent example is China where the ratio is going to increase from 17% to 44%. For industrialized countries, however, the absolute level of this ratio is the main reason for concern, reaching, for example, 51% in Western Europe.

This development is reflected in the first pillar of the API, called the starting points, which combines demographic change and the public financial situation (financial leeway). Not surprisingly, many emerging countries in Africa score rather well as the population is still young and public deficits and debts are rather low. On the other hand, many European countries such as Italy or Portugal are among the worst performers: Old populations meet high debts. “For most industrialized countries, the old Scottish joke applies: If I were to build a stable pension system, I certainly wouldn’t start from here”, said Michaela Grimm, Allianz economist and author of the report. “And that is the situation before the coronavirus and its tsunami of new debt. One of the legacies of the current crisis will certainly be that we have to double our efforts to reform our pension systems. What had remained of financial leeway has gone for good.”

The second pillar of the API is sustainability, measuring how systems react to demographic change: Are there built-in stabilizers or will the system be blown apart when the number of contributors falls while that of beneficiaries keeps rising? In that context, an important lever is the retirement age. In the 1950s, an average 65-year old men, living in Asia could expect to spend around 8.9 years in retirement (women 10.3 years). Today, the average further life expectancy of a 65-year old is 17.8 years for women and 15.2 years for men and it is set to increase to 19.9 years (women) and 17.5 years (men) respectively in 2050. As a consequence, the ratio of working life to time spent in retirement has declined markedly. Countries, which decided to adjust the legal retirement age or the increase of pension benefits to the development of further life expectancy like the Netherlands, have thus a more sustainable pension system than countries where postponing retirement further is still a taboo.

The third pillar of the API rates the adequacy of a pension system, questioning whether it provides an adequate standard of living in old age. Important levers are the coverage ratio – i.e. how big are the shares of the working age population and the age group in retirement age that are covered by the pension system? –, the benefit ratio – i.e. how much money (measured in terms of average income) does an average pensioner receive? –, and last but not least the existence of capital-funded old-age provision and other sources of income. Overall, the average score in the adequacy pillar (3.7) is slightly better than that in the sustainability pillar (4.0), a sign that most systems still put greater weight on the well-being of the current generation of pensioners than on that of the future generation of tax and social contribution payers. The countries leading the adequacy ranking have either still rather generous state pensions, like Austria or Italy, or strong capital-funded second and third pillars, like New Zealand or the Netherlands.

However, capital-funded retirement solutions are under increasing pressure in the persisting low interest rate environment. The COVID-19 pandemic has further exacerbated this trend by further pushing down yields. “The low yield environment has forced both pension funds and life insurers to explore alternative asset classes”, said Cameron Jovanovic, head of global retirement proposition at Allianz SE. “This push into alternatives enables benefit providers to capture the illiquidity premium that matches well with their portfolio duration. Another strategy is to offload risk rather than chasing returns as longevity swaps, pension risk transfers and creative reinsurance set-ups become means of optimizing the exposure taken on by pension funds and insurers.”

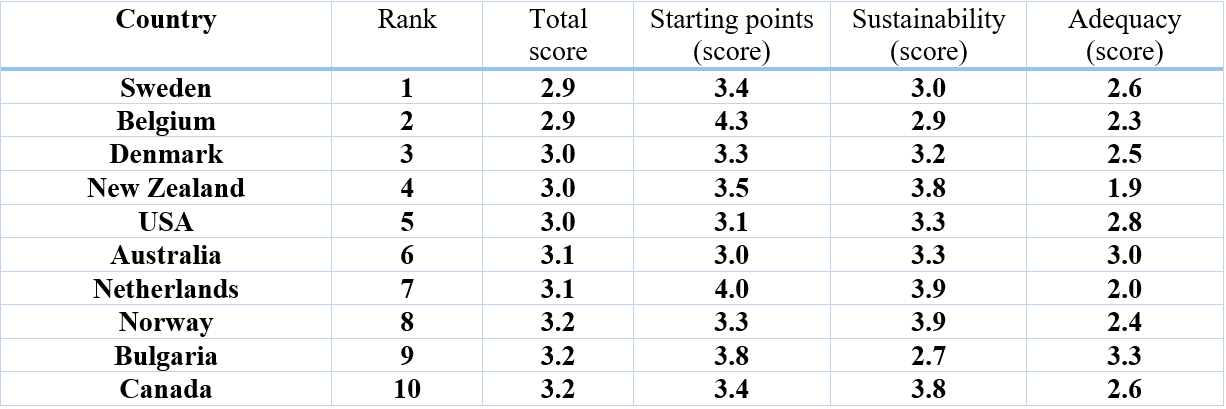

Combining the scores of all three pillars of the API gives the overall results: Sweden, Belgium, and Denmark come out as the relatively best pension systems worldwide (see table).

There is no Asian market among the top-10. This comes not as a surprise. The region is especially hard hit by aging, with only a few exceptions (India, Laos and the Philippines). But there are also some bright spots. China and Indonesia for example, have decided to raise the retirement age significantly. Four markets, China, Japan, South Korea and Taiwan have already included a demographic factor in their pension formula. As a result, Indonesia, China and South Korea are among the top-10 in the sustainability rankings. Singapore and Japan, on the other hand, boast a wide coverage in their first pillar and built a strong second pillar; thus, both markets rank among the top-5 in the adequacy ranking. Overall, however, currently China’s pension system is the best-prepared for the upcoming demographic change, ranking at #11 in the global list. But most other Asian markets have still homework to do to make their systems demography-proof.

[1] People aged 65 and older in percentage of people aged between 15 and 64.

Top ten pensions system worldwide

Top ten pension systems in Asia

You can find the study here on our homepage