- Strong growth: The global premium pool grew by +4.9% in 2022 – against the backdrop of a global inflation rate of 8.6%

- America's dominance, China’s rise: North America’s global market share stood at 43.9% while China was able to almost double its share to 11.4%

- Anchor in turbulent times: Insurance is an essential shock absorber, as it flattens the curve of the economic cycle

- Continuity at the surface: Premiums are set to increase by 5.2% p.a. over the next decade, adding EUR4,190bn to the global premium pool

- Transformation beneath: The business model of insurers will evolve, from pure financial compensation to risk management and prevention

Today, Allianz published its latest “Global Insurance Report”, which analyzes the development of insurance markets worldwide[1].

Strong growth

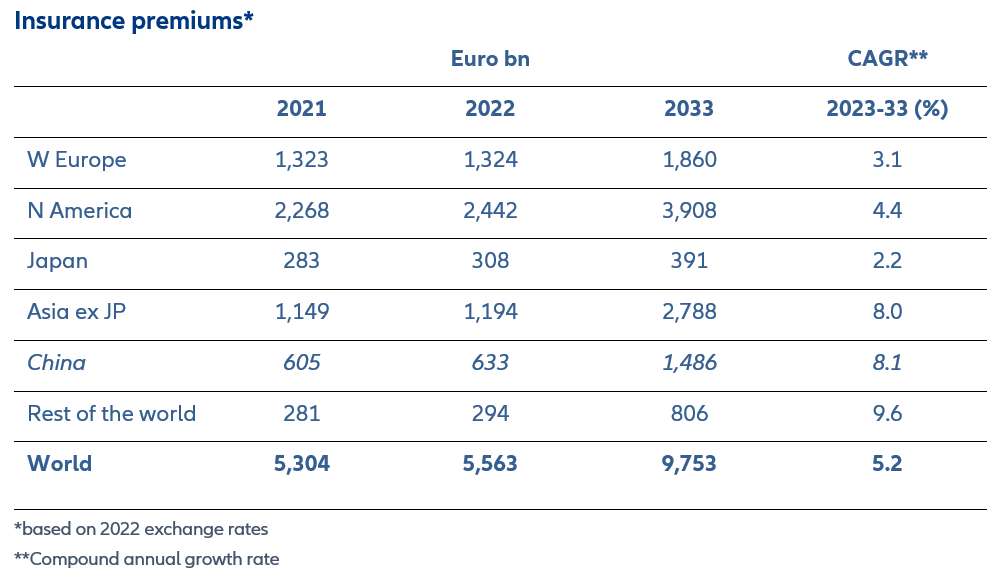

According to the report, total global insurance premium income amounted to almost EUR5.6trn in 2022. Life remains the largest segment (EUR2.6trn), ahead of property & casualty (p&c) (EUR1.8trn) and health (EUR1.1trn). In 2022, the premium pool grew by EUR259bn or +4.9% – against the backdrop of a global inflation rate of 8.6%. The three segments, however, fared very differently: while p&c clocked robust growth of +8.7%, health expanded by more modest +4.9%, and life insurance market growth was a dismal +2.4%: squeezed real households’ incomes took the toll on private savings.

The rise in p&c premiums was driven by all regions around the globe. However, with EUR77.5bn (+9.9%), more than half of the global increase in 2022 came from North America alone; with premium income of EUR860bn, the region remains by far the largest market worldwide. Asia, too, saw healthy growth of 8.4% last year (+EUR31bn). With total premium income of nearly EUR403bn, the region overtook Europe for the first time (+4% or EUR15bn to EUR397bn).

Life insurance markets suffered last year, particularly in Western Europe: premium income declined by 2.7% in 2022 (-EUR21bn to EUR740bn). Growth was disappointing in Asia, too, recording a modest increase of +3.6% (+EUR33bn to EUR952bn). As in p&c, North America was the main growth driver in 2022, with +7.8% or EUR61bn to EUR840bn. America’s dominance is even more pronounced in health where the US market accounts for around two thirds of all premium income worldwide.

America’s dominance, China’s rise

North America – i.e., the US, which accounts for 94% of the region’s premium pool – dominated the global insurance market not only in 2022, but over the last decade: More than half of the increase in global premium income in p&c and health was generated there. In life, the share is still slightly below one-third, while Asia commands the biggest slice of the cake. As a result, the region’s global market share rose from an already impressive 39.6% in 2012 to a whopping 43.9% in 2022. This is in sharp contrast to Western Europe, which lost more than 6pps to reach 23.8%. The other clear “loser” is Japan (-3.7pps to 5.5%), while China was able to almost double its global share to 11.4%; the rest of Asia stood at 10.1%.

Anchor in turbulent times

In economic terms, navigating an inflationary environment will be the biggest challenge in the coming years. Five structural drivers will determine inflation, the "Five Ds": demographics, deglobalization, decarbonization, digitalization and debt. Overall, the five Ds might significantly lift annual inflation by up to 1 percentage point. “Insurance proves its worth in turbulent times of high inflation and low growth.”, said Ludovic Subran, chief economist of Allianz. “The insurance industry cannot undo inflation, but it can smooth out the impact over time, acting as a kind of buffer. According to Eurostat, for instance, inflation in personal p&c insurance like motor and property trailed headline inflation by a wide margin last year. Insurance is an essential shock absorber, as it flattens the curve of the economic cycle for its customers.”

Continuity at the surface

Despite higher inflation – or perhaps precisely because of it – premiums are set to increase by 5.2% over the next decade, adding EUR4,190bn to the global premium pool. In 2033, premium income will reach EUR4.3trn in life, EUR3.1trn in p&c and EUR2.3trn in health.

With EUR1.726bn, most of the increase will be in the life segment. However, annual growth (+4.7%) over the next decade is likely to lag well behind general economic growth (+5.2%). Insurance penetration will thus fall by 3pp to 2.8%. Asia will remain the growth engine for global life business, with annual growth (ex Japan) expected to rise to 7.5%. The region should account for the half of absolute premium growth (EUR866bn), more than North America (EUR377bn) and Europe (EUR276bn) combined.

In the p&c segment, additional premiums will amount to EUR1.282bn by 2033. This represents an annual growth rate of 5.0%, roughly in line with the previous decade (5.1%) and general economic growth (5.2%); insurance penetration will therefore decrease only slightly by 1pp (to 2.0%). As in the life segment, Asia (excluding Japan) is the clear growth champion among the major regions with an annual rate of +8.1%. In absolute terms, however, the importance of the region is lower than in the life segment: "only" around 35% of the expected premium growth (EUR448bn) is attributable to Asia, against EUR357bn in North America and EUR168bn in Europe.

In Germany, insurance premium are expected to increase by 2.8% p.a.; total market size will reach EUR296bn in 2033. With that, Germany will remain among the top10 insurance markets worldwide at #8. Life is likely to remain the biggest segment (EUR118bn), followed by p&c (EUR113bn) and health (EUR65bn).

Transformation beneath

In view of the major technological upheavals and new and rising risks, this forecast – which suggests more or less continuity – may come as a surprise. However, this applies only to the surface of premium growth. The underlying changes are dramatic.

Technology will change how insurers operate. Ecosystems, for instance, will play a decisive role in customer access, offering not only individual products, but comprehensive solutions for customer needs, be it for mobility, living, travel, wealth, or health. AI opens unimagined possibilities in data analytics, revolutionizing the entire value chain from underwriting to claims handling.

“Preserving its social relevance, the industry is facing a fundamental change in its business model.”, said Michaela Grimm, co-author of the report. “The value proposition of insurers will evolve, from pure financial compensation to risk management and holistic service offerings to prevent and mitigate risks. This follows an inescapable logic: to close the huge protection gaps – in natcat, cyber, health or pension – mobilizing more premiums might not be enough; avoiding risks in the first place becomes more and more important.”

[1] All figures are based on 2022 exchange rates.

For further information please contact:

Allianz Asia Pacific

Noridahwati Razak, +65 9725 3865, noridahwati.razak@allianz.com.sg